S. Gechert, D. Guarascio, P. Heimberger, B. Schütz, F. Zezza – 15th October 2024

EU fiscal rules: time to face the contradictions

D. Guarascio, F. Zezza – 13th December 2023

Un’analisi critica della proposta di riforma delle regole fiscali europee

D. Guarascio, F. Zezza – 18 Dicembre 2022

Il Recovery Plan, il Sud e le promesse mancate

F. Zezza – 4 Maggio 2021

Italia: arriverà la ripresa?

Dimitri B. Papadimitriou, Francesco Zezza, Gennaro Zezza – 12 Ottobre 2020

Short note on Italian labour market

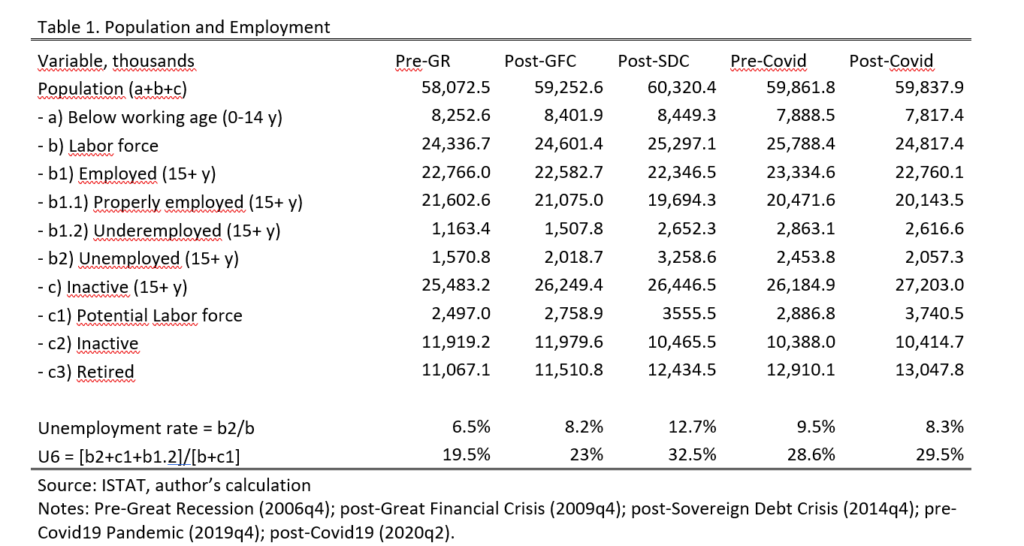

More than a decade passed since the outbreak of the Great Recession of 2007-08 but, at the onset of the Covid19 Pandemic Crisis, Italy had not yet recovered its pre-crisis GDP levels. A central role in the under-performance of the country has been played by labour market dynamics. Table 1 records the decomposition of the Italian population, combining ISTAT employment and “complementary indicators” data.

Total population can be split between those “below working age” (a) and “15-years or older”. The second group is then split between labour force (b) and inactive population (c). Inside the labour force, we can distinguish between employed (b1) and unemployed (b2) and, in the former group, those “involuntary employed part-time” (b1.2). Finally, the inactive population can be split between “potential labour force”, “inactive”, and “retired” (c1, c2, and c3 respectively).

Using these sources, we can compute the unemployment rate – i.e., the ratio between the unemployed and the labour force – as well as the U6 measure of unemployment. The latter is computed by adding – to both the numerator and denominator – the potential labour force and adding the underemployed to the numerator.

The sharp increase in underemployment – from 1.1 to 2.8 million between 2006 and 2019 – caused the U6 measure to peak at an extraordinary 32.5 percent by the end of Sovereign Debt Crisis and to keep it at high levels in the run up to the Covid19 Pandemic. Using the broader definition of unemployment, thus, the number of non-occupied workers increased by 4.2 million – compared to the 1.8 million increase in unemployed.

The recovery in employment has been the outcome of a reallocation of the labour force towards low-skilled (and low wages) sectors. Figure 1 reports the absolute changes in employment by type of industry, for the period 2007-2019.

By the end of 2019, employment in construction was still 30 percent below its peak in 2007 (-580 thousand workers), while industry was still down by 6 percent (-304 thousand). The performance in services (+6 percent, equal to 1.3 million workers) was mainly led by accommodation and catering services, driven by the growth in the tourism industry.

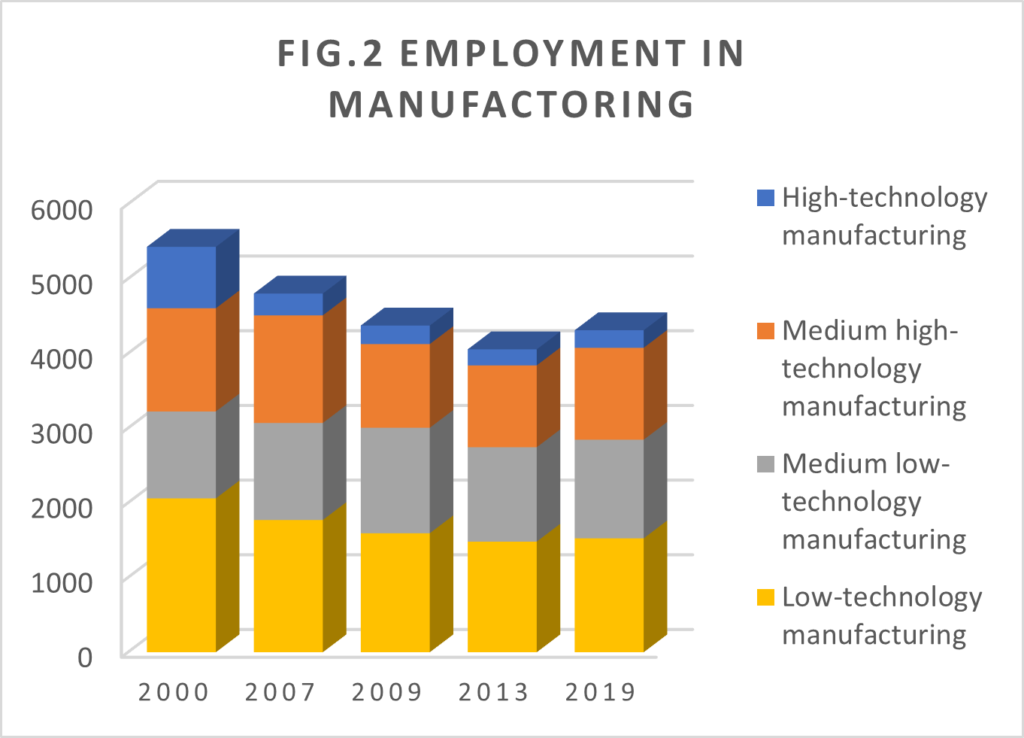

Inside the manufacturing sector, a positive sign was represented by the recent increase in the number of workers employed in high and medium-high technology industries, led by the incentives related to Industria4.0.

It should be noted, however, that figures are still way below their levels at the onset of the last decade, where high-tech manufacturing workers accounted for 15 percent of industrial employment (Figure 2).

In February 2020, the first Covid19 cases where reported, and soon the death toll and the pression on the NHS surged, leading the Government to adopt extraordinary measures the counteract the pandemic.

The impact of the Pandemic on the Labour market

Italy was the first western country to be severely hit by the Covid19 pandemic, and the first one to adopt complete lockdown measures between April and June. The shutdown was gradually relaxed in the summer, even though some service activities continued to operate with restrictions.

The lockdown led to the largest drop in quarterly GDP the country has ever experienced, with a (year-on-year) -5.6 percent in Q1 and an unprecedented -17.7 in Q2. In the second quarter domestic demand collapsed by 9.7 percent, driven by falls in consumption (8.7 percent) and investment (14.9 percent), while net external demand dropped by 2.4 percent (-26.4 percent in exports and -20.5 percent in imports).

This was, by far, the largest drop in production recorded for Italy since the start of the quarterly GDP series in 1995: in 2009Q1, GDP decreased “only” by 2.8 percent.

As reported by ISTAT in its annual report on the Italian economy, between March and May 2020, 45 percent of firms suspended their activities due to the government restrictions, with even higher percentage among SMEs. However, the 30 percent of (mostly large) firms that remained open throughout the crisis, still accounted for over 60 percent of total domestic production.

Due to the restrictions on activity related to the lockdown measures, the industrial production index hit its historical minimum in April, at 59.4.

Value-added dropped in all industrial sectors in the two following months: 22 percent in construction, 19.8 percent in industry, and 11 percent in services. Although there has been great heterogeneity among sectors, provisional monthly data display a partial recovery throughout the summer.

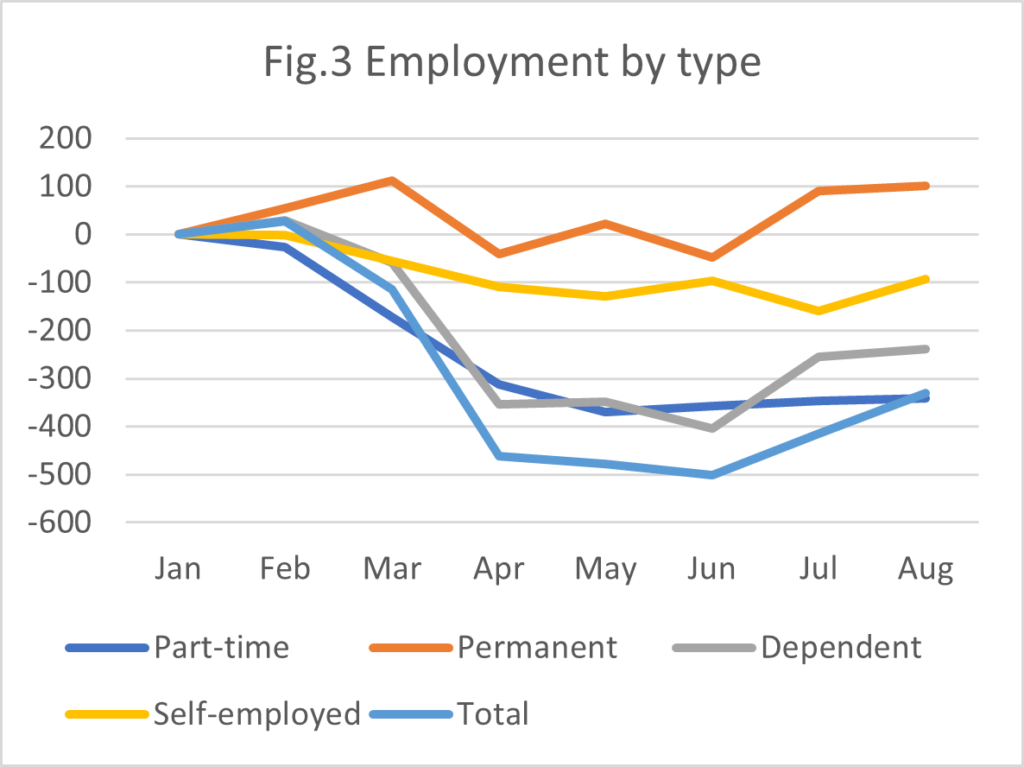

The fall in the service sector can also be interpreted by looking at monthly employment data in Figure 3.

Most of the fall in employment is indeed due to the drop in part-time workers – which characterizes most services, and in particular those more severely hit by the restrictive measures, i.e., restoration, accommodation and entertainment.

To the drop in labour force corresponded a large increase in the inactive population – which peaked in April at 1-1 million. In the second quarter the number of unemployed turned back to its pre-crisis level, also because more people gained access to unemployment insurance schemes. Consequently, between January and June the unemployment rate fell by 1.2 percent, while the U6 increased by 0.9.

Along with the measures adopted to contain the spread of the virus and to further support the NHS, the Government intervened with four Decrees from the Prime Minister (DPCM), aimed at mitigating the impact of the crisis on the private sector, totalling 100 billion in additional outlays for 2020.

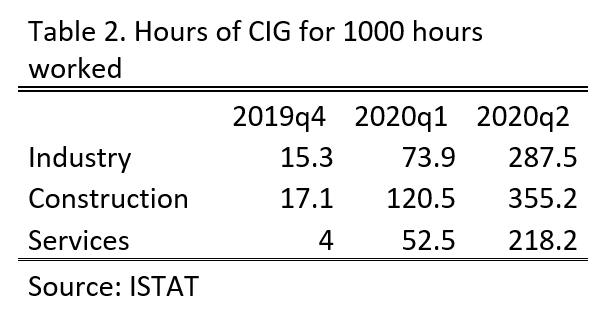

A central role in toning down the impact of the pandemic on the labour market has been certainly played by the Government decision to impose, on the one hand, layoff restrictions for all firms accessing restoring measures, and, on the other, to increase the funding for Cassa Integrazione (for a total of 19.1 billion) and extend the eligibility criteria to gain access to the scheme. Table 2 reports indeed the number of hours of CIG for every thousand hours worked, displaying the large increase for all sectors in the first two quarters of the year. It should be noted, however, that due to the large increase in applications and the complex procedures involved, there have been large delays in payments in the first months: as of the end of May only half the accepted applications were paid.

The situation improved sensibly when the Government introduced a simplified procedure to access the scheme in late May: by mid-October, only 2 percent of processed applications are still undue.

However, while both measures are intended to last until the end of the year, it is almost certain that the government would have to intervene again, especially in light of the new measures introduced in late October, that again restrain the opening hours and impose restrictions on mobility, along with the complete shutdown for some specific service sectors.

The unprecedented severity of the economic crisis calls for extraordinary measures: not only the safety nets already in place should be extended and maintained, but of the upmost importance is to set up structural measures to absorb the unemployed and, even more so, the large number of (young) inactive and discouraged, whose numbers are sadly going to further increase.

As discussed elsewhere, the first direction should be to directly increase Public Sector employment. To re-align public employment to the EU average, public employment should expand by about 40 percent, i.e., approximately 1.4 million workers. A program of this sort should be primarily aimed at lowering the average age of public sector employees – which is higher in Italy with respect to the rest of EU. A younger – and more qualified – PA would ease the digitalisation of public services, while large investments in public and private knowledge-intensive sectors (R&D, Education, NHS, Green Economy) would help boost productivity – which has been stagnant in the last three decades.

Along the direct employment in the public sector, it will be central to further enhance programs of “trace, track and treat” of newly unemployed workers – such as the Reddito di Cittadinanza – aimed at easing the search for jobs and develop the skills and qualifications needed.

However, if the Government does not intervene promptly and adequately, the Pandemic crisis will surely bear long-lasting effects on labour market and the industrial structure of the country, curtailing future growth prospects, and leaving the restoration of pre-GFC GDP levels as a mere vision.